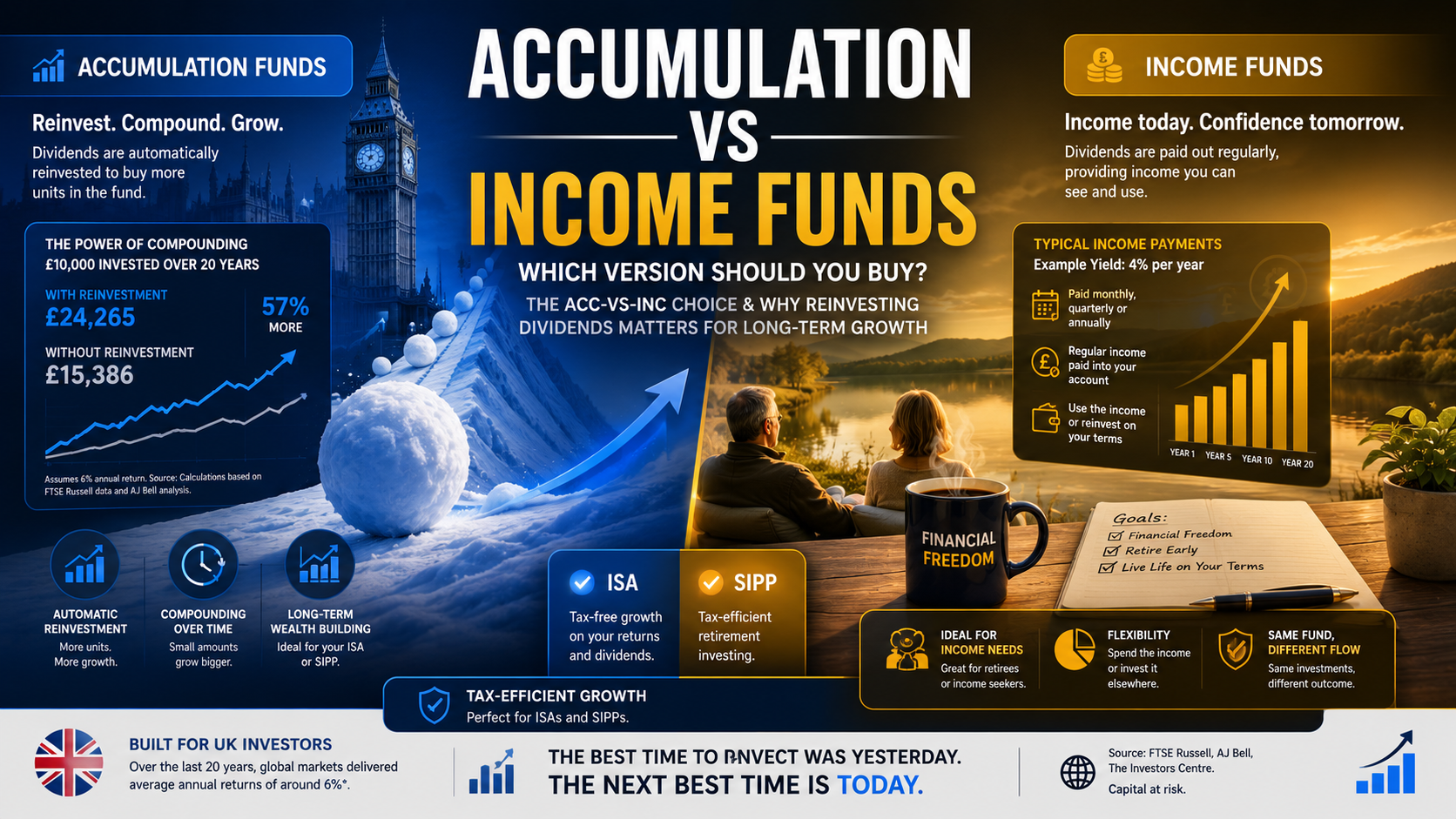

For many UK investors, choosing an index fund feels surprisingly difficult. A quick online search produces dozens of "best index fund" lists, each claiming a different winner. The reality is that there is no universally best index fund. The right choice depends on a handful of practical factors that matter far more than short-term performance tables.

If you are starting your investing journey through a Stocks and Shares ISA or SIPP, the most important decision is not finding the latest top performer. It is selecting a low-cost, diversified global tracker that you can comfortably hold for years, or even decades.

This guide focuses on the criteria that genuinely matter when comparing global index funds, including costs, diversification, fund size and platform availability.

Why Global Tracker Funds Are Popular With UK Investors.

Global tracker funds have become increasingly popular because they offer exposure to thousands of companies around the world through a single investment. Instead of trying to pick individual shares or sectors, investors simply buy the market.

The trend towards passive investing continues to grow. According to Investment Association data, index funds now account for around 35% of UK assets under management, the highest level on record. This reflects growing demand for low-cost investment solutions.

Passive investing has also gained support because many actively managed funds struggle to outperform their benchmark indexes after fees. Long-term SPIVA studies regularly show that most active managers underperform over extended periods.

For beginners, that makes global trackers an attractive starting point.

The Three Factors That Actually Matter.

When comparing global index funds, there are three core areas worth focusing on.

Cost.

The ongoing charges figure, often called the OCF, is the annual fee charged by the fund.

The difference between a 0.10% fund and a 1.00% active fund may not sound significant, but over decades those costs compound. Many popular global tracker funds now charge between 0.12% and 0.23% annually, while active funds often charge around 0.75% or more.

A lower fee is generally better, provided the fund still delivers the diversification you need.

Breadth Of Diversification.

A global tracker is only as global as the index it follows.

Some funds track developed markets only. Others include both developed and emerging markets. Some include small companies while others focus solely on large and medium-sized firms.

Broader diversification means your portfolio is less dependent on the fortunes of any single country or region.

For example, a truly global fund can provide exposure to thousands of companies across North America, Europe, Asia-Pacific and emerging markets.

Fund Size.

Large funds tend to offer better liquidity and operational stability.

While a small fund is not automatically a bad choice, many investors prefer established funds with billions of pounds under management and a long track record.

Large funds are also less likely to be merged or closed in future.

Comparing Popular Global Index Funds.

Rather than producing another "best funds" ranking, it is more useful to compare some of the most commonly chosen options available to UK investors.

Vanguard FTSE Global All Cap Index Fund.

This is often considered one of the broadest global tracker funds available to UK retail investors.

The fund tracks developed and emerging markets and includes large, medium and small-cap companies. It provides exposure to more than 7,000 stocks worldwide and carries an ongoing charge of approximately 0.23%.

For investors who want maximum diversification through a single fund, it remains one of the strongest options available.

HSBC FTSE All-World Index Fund.

The HSBC FTSE All-World Index Fund is another popular choice.

It includes developed and emerging markets but focuses primarily on large and medium-sized companies. The ongoing charge is around 0.13%, making it significantly cheaper than some competitors.

Investors seeking a balance between low cost and broad global exposure often shortlist this fund.

Fidelity Index World Fund.

Fidelity Index World tracks developed markets only and excludes emerging markets.

The fund holds roughly 1,500 companies across developed economies and charges around 0.12% annually.

While highly competitive on cost, investors wanting complete global coverage may choose to combine it with a separate emerging markets fund.

Vanguard FTSE All-World ETF (VWRP).

For investors comfortable using ETFs, VWRP is one of the most widely used global options.

The fund tracks approximately 3,700 large and medium-sized companies across developed and emerging markets and carries a charge of around 0.22%.

Many UK investors appreciate the ETF structure, particularly on platforms that offer low-cost ETF investing.

Why Fund Performance Should Not Be Your Main Focus.

One of the biggest mistakes beginners make is choosing a fund based on recent returns.

The problem is that most global trackers investing in similar markets will deliver broadly similar performance over the long term.

Differences in returns often come down to temporary market conditions rather than superior fund selection.

For example, a fund with heavier US exposure may outperform during a strong period for American technology stocks. A different fund may lead when emerging markets are performing well.

Instead of chasing last year's winner, investors are generally better served by focusing on costs, diversification and consistency.

Platform Fees Matter More Than Many Investors Realise.

Many beginners spend hours comparing funds while overlooking platform costs.

In reality, platform fees can have just as much impact on long-term returns as fund charges.

Popular UK investment platforms include:

- Vanguard Investor

- AJ Bell

- Hargreaves Lansdown

- Interactive Investor

- InvestEngine

Each platform uses a different charging structure. Some charge percentage-based fees while others charge fixed monthly fees.

For smaller portfolios, percentage-based pricing may be cheaper. Larger portfolios often benefit from flat-fee providers.

This is where many investors can save more money than they would by endlessly comparing similar tracker funds.

Should You Choose A Global Fund Or A UK Fund.

Many new investors naturally feel more comfortable investing in UK companies.

However, the UK stock market represents only a small portion of the global equity market.

A global tracker provides exposure to major international businesses including Apple, Microsoft, Nvidia, Nestlé, Toyota and thousands of others.

While UK-focused funds can still play a role, concentrating entirely on domestic shares increases risk through a phenomenon known as home bias.

Diversification across global markets remains the approach preferred by many long-term passive investors.

Index Funds Inside An ISA.

For most beginners, a Stocks and Shares ISA is often the most tax-efficient home for index fund investments.

All capital gains and investment income generated inside the ISA remain free from UK income tax and capital gains tax. The current annual ISA allowance remains £20,000.

Combining a global tracker fund with a Stocks and Shares ISA creates a simple and tax-efficient foundation for long-term wealth building.

The Simpler Choice Is Often The Better Choice.

Many investors spend weeks trying to identify the perfect index fund.

In reality, the difference between several well-diversified global trackers is often relatively small compared with the benefits of investing consistently over time.

A low-cost global tracker held inside a Stocks and Shares ISA and funded regularly is often enough to build substantial wealth over the long term. As many experienced investors point out, consistency tends to matter far more than optimisation.

Rather than searching for a magic fund, focus on finding a diversified global tracker with reasonable costs, a strong track record and availability on a platform that suits your needs. Then concentrate on the one factor that ultimately drives results: staying invested.

Want help getting started? Subscribe today and claim your free copy of the Investing for Beginners Handbook packed with practical investing tips for UK beginners.