Choosing a fund is often seen as the difficult part of investing. Yet many investors overlook another important decision that appears after selecting a fund. Should you buy the accumulation version or the income version?

This seemingly small choice can have a significant impact on how your investments grow over time, how much administration you face, and whether your portfolio aligns with your financial goals.

The accumulation versus income fund debate is particularly relevant for UK investors using ISAs, SIPPs and general investment accounts. While both versions invest in exactly the same underlying assets, the way they handle dividends and interest payments is very different.

Understanding how these share classes work can help you make a more informed investment decision and potentially improve your long-term returns.

What Are Accumulation And Income Funds?.

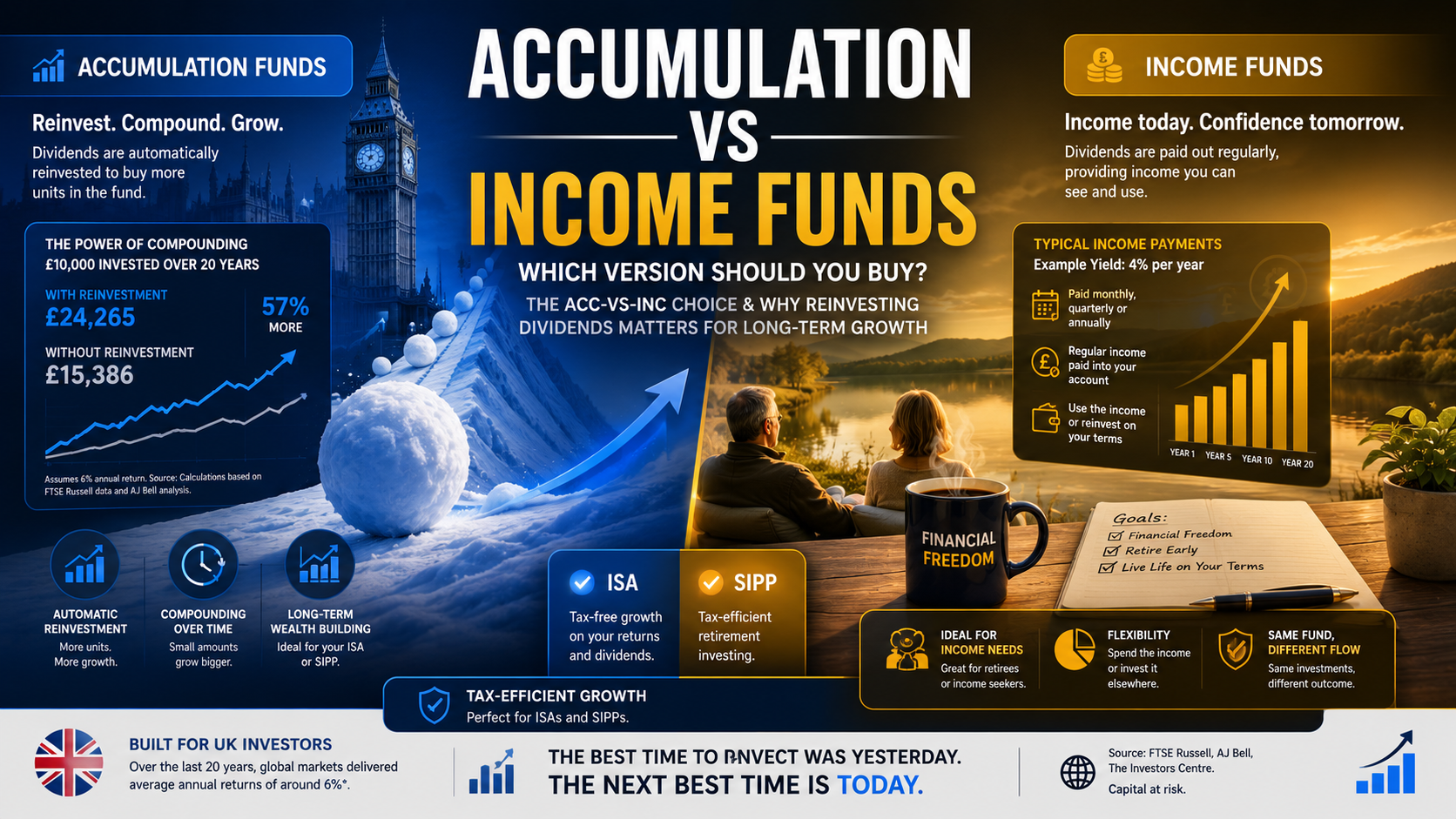

Many UK funds are available in two share classes, often identified by the abbreviations "Acc" and "Inc".

An accumulation fund automatically reinvests any dividends or income generated by the investments held within the fund. Instead of receiving cash payments, the income remains invested and contributes to the overall growth of the fund.

An income fund distributes the income generated by the underlying investments directly to investors. Depending on the fund, these payments may be made monthly, quarterly, semi-annually or annually.

Importantly, both versions invest in the same portfolio and follow the same investment strategy. The only difference is what happens to the income produced by the holdings.

Why Reinvesting Dividends Matters So Much Over Time.

One of the biggest advantages of accumulation funds is the power of compounding.

When dividends are reinvested automatically, future returns are earned not only on the original investment but also on previous dividends. This creates a snowball effect that becomes increasingly powerful over long periods.

For example, an investor who earns a 4% annual dividend yield and reinvests those payments can potentially generate substantially higher returns over 20 or 30 years than someone who withdraws the income.

This principle is one reason why many pension investors favour accumulation funds during their working years. Every dividend remains invested and continues working towards future growth.

Many of today's ISA millionaires achieved their wealth through decades of consistent investing and compounding rather than short-term market timing. Recent platform data showed significant growth in the number of ISA millionaires following strong market performance and long-term investment discipline.

When Income Funds Make More Sense.

Despite the benefits of compounding, accumulation funds are not automatically the right choice for everyone.

Income funds are often preferred by investors who rely on their portfolios to generate cash flow. Retirees, semi-retirees and those pursuing income-focused strategies may value receiving regular payments without having to sell investments.

An income fund allows investors to receive dividends directly into their account while keeping the underlying investment intact. This can create a more predictable source of income and simplify budgeting during retirement.

Some investors also prefer income share classes because they want flexibility. Rather than automatically reinvesting dividends back into the same fund, they may choose to invest the income elsewhere or hold it in cash for future opportunities.

The Real Difference In Long-Term Returns.

Many investors assume accumulation and income funds generate different investment returns. Technically, they do not.

The underlying investments are identical.

However, the investor experience can be very different.

If an investor spends the income generated by an income fund, their total portfolio growth will generally be lower than someone who reinvests every dividend through an accumulation fund.

The difference becomes more pronounced as the investment period increases. Over a decade or more, reinvested dividends can contribute a substantial portion of overall investment returns.

This is especially important for younger investors building wealth for retirement, financial independence or long-term financial goals.

Which Option Is Best For ISA Investors?.

For many Stocks and Shares ISA investors, accumulation funds are often the default choice.

The UK ISA market reached a record value of approximately £872 billion, highlighting the growing popularity of tax-efficient investing among British savers.

Because ISAs shelter investors from dividend tax and capital gains tax, many people use them as long-term wealth-building vehicles. In these circumstances, automatic dividend reinvestment can help maximise growth while reducing administration.

Investors saving for retirement, financial independence, children's future expenses or other long-term goals often find accumulation funds a convenient solution.

However, investors who are already living off their portfolios may prefer income share classes even within an ISA because they provide a straightforward way to generate regular tax-free income.

Which Option Is Best For SIPP Investors?.

For pension investors, accumulation funds are often particularly attractive.

Most SIPP investors are building retirement wealth over many years and do not need immediate access to investment income. Automatic reinvestment allows contributions and dividends to remain invested and benefit from compounding.

The UK continues to see substantial pension participation, with workplace pension contributions reaching nearly £150 billion annually, reflecting the importance of long-term retirement planning.

Once retirement arrives, some investors switch from accumulation units to income units as part of a broader income-drawing strategy.

This transition can help create a more predictable income stream without requiring frequent sales of fund units.

Tax Considerations Investors Should Understand.

A common misconception is that accumulation funds avoid taxation because income is not physically paid out.

That is not the case.

Outside an ISA or pension wrapper, HMRC generally treats accumulated income similarly to distributed income for tax purposes. Investors may still have tax reporting obligations even when income remains within the fund.

This is one reason why ISAs and SIPPs remain popular choices for fund investing.

Within these tax-efficient accounts, investors generally avoid UK income tax and capital gains tax on investment growth and distributions.

For investors using general investment accounts, understanding the tax treatment of accumulation units is essential before making a decision.

How To Identify Acc And Inc Share Classes.

Fortunately, fund providers make it relatively easy to distinguish between the two options.

Accumulation share classes usually include:

- Acc

- Accumulation

- Growth

- Capitalising

Income share classes often include:

- Inc

- Income

- Distribution

- Distributing

Before investing, it is worth checking the fund factsheet or platform description to confirm which share class you are selecting. A surprising number of investors accidentally purchase the wrong version simply because they overlook the share class designation.

A Simple Rule For Choosing Between Them.

For most investors, the decision comes down to one straightforward question.

Do you need the income today?

If the answer is no, accumulation funds will often be the more suitable option because they allow dividends and interest payments to remain invested and compound automatically.

If the answer is yes, income funds may provide a convenient way to generate cash flow without regularly selling investments.

Neither option is universally better. The right choice depends entirely on your goals, time horizon and income requirements.

What matters most is understanding the difference and ensuring your chosen share class supports your wider investment strategy.

Why This Decision Matters More Than Many Investors Realise.

The accumulation versus income fund choice rarely attracts the same attention as stock picking, fund selection or market forecasts. Yet it can have a meaningful effect on how wealth is built and managed over time.

For long-term investors focused on growth, accumulation funds offer a simple and effective way to harness the power of compounding. For those seeking regular cash flow, income funds provide a practical solution without changing the underlying investment strategy.

In many cases, the smartest approach is not asking which share class is better, but which share class is better for your current stage of life.

For more beginner-friendly investing guides, subscribe today and claim your free copy of the Investing for Beginners Handbook eBook.