For many UK investors, building wealth is often made to seem far more complicated than it needs to be. Financial media, investment platforms and social media influencers regularly discuss individual shares, market predictions and complex strategies. Yet some of the most successful long-term investors follow a much simpler approach.

A straightforward portfolio built from one global fund or a small collection of index funds can provide broad diversification, low costs and an easy-to-manage investment strategy. It is also an approach that aligns with what many financial planners recommend for long-term investors who want to focus on growing wealth rather than constantly monitoring markets.

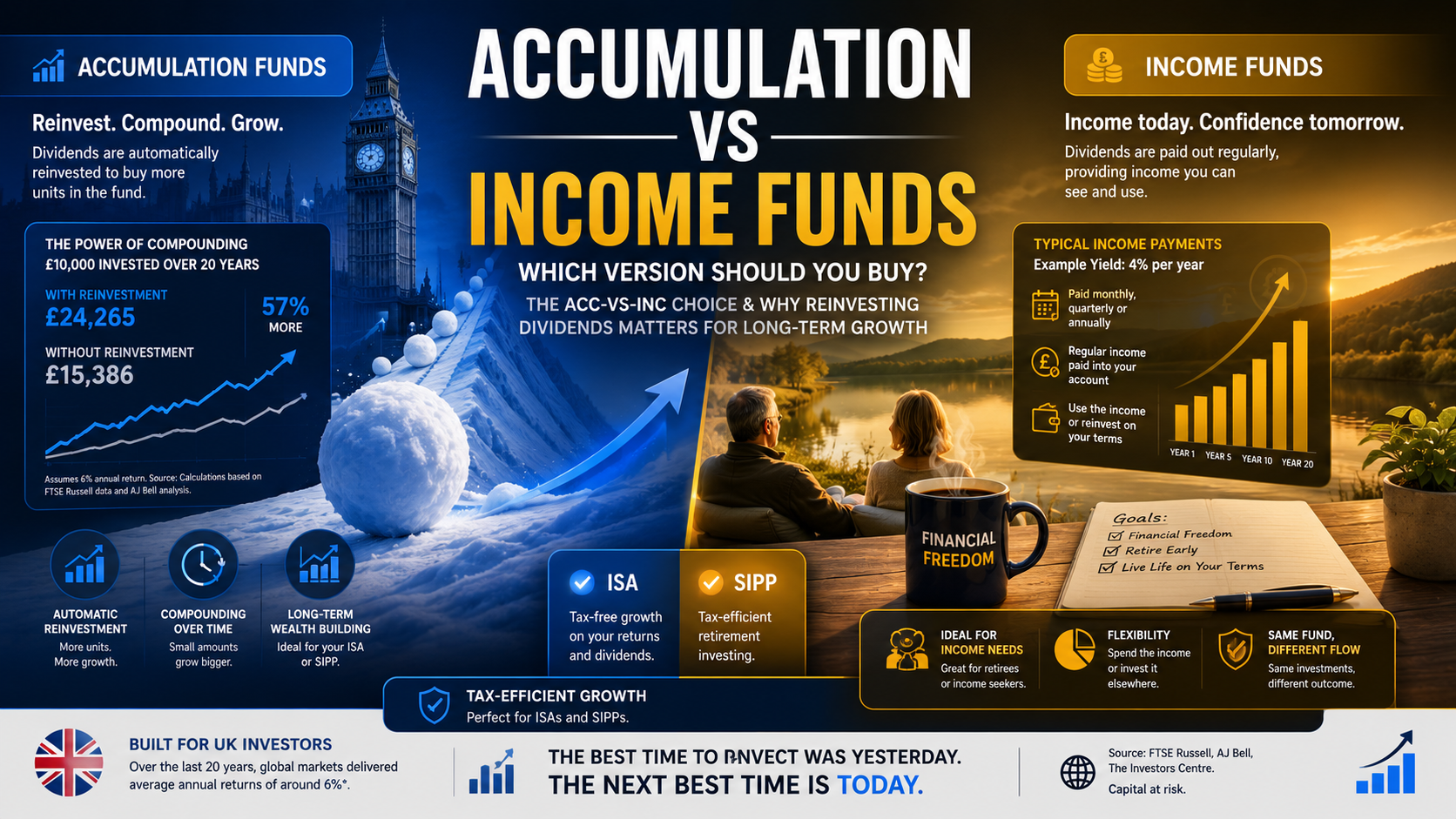

Whether you are investing through a Stocks and Shares ISA, a SIPP or a workplace pension, understanding how to construct a sensible portfolio is one of the most important investing skills you can learn.

Why Asset Allocation Matters More Than Fund Selection.

Many new investors spend hours researching individual funds while paying little attention to the overall mix of shares and bonds within their portfolio. However, decades of investment research suggest that asset allocation is one of the biggest drivers of long-term returns and volatility.

Asset allocation simply refers to how your investments are divided between different asset classes such as equities and bonds.

Equities have historically generated higher long-term returns but experience greater short-term volatility. Bonds typically provide lower returns but can help smooth portfolio performance during market downturns.

The challenge is finding a balance that allows you to stay invested during periods of market turbulence while still achieving your long-term goals.

This has become increasingly important as more Britons invest for their future. According to the latest workplace pension data, around 82% of UK workers now participate in a workplace pension scheme, representing approximately 23.3 million employees. Auto-enrolment has significantly increased the number of people investing for retirement over the past decade.

The Simplest Option - A One-Fund Portfolio.

For many investors, a single globally diversified fund may be all that is required.

A one-fund portfolio typically consists of a global index fund that invests across thousands of companies worldwide. Instead of choosing individual regions or sectors, investors gain exposure to markets across North America, Europe, Asia and emerging economies through a single investment.

Popular examples available to UK investors include:

- Vanguard FTSE Global All Cap Index Fund

- HSBC FTSE All World Index Fund

- Fidelity Index World Fund

- Vanguard LifeStrategy Funds

The key advantage is simplicity. You make regular contributions, reinvest dividends and allow the fund manager to handle the underlying portfolio management.

Many investors discover that the hardest part of investing is not selecting investments but maintaining discipline. A one-fund solution removes much of the temptation to tinker with your portfolio.

Building a Traditional Three-Fund Portfolio.

For investors who want slightly more control over asset allocation, a three-fund portfolio is often considered the gold standard of passive investing.

The concept originated in the United States but adapts well to UK investors.

A typical UK three-fund portfolio could consist of:

1. Global Equity Fund.

This forms the growth engine of the portfolio.

Examples include:

- Vanguard FTSE Global All Cap Index

- HSBC FTSE All World Index

- iShares MSCI ACWI ETF

A global equity fund provides exposure to thousands of companies across developed and emerging markets.

2. UK Bond Fund.

Bonds help reduce portfolio volatility and provide stability during periods of market stress.

Examples include:

- Vanguard UK Government Bond Index Fund

- iShares UK Gilts ETF

- Vanguard Global Bond Index Fund

Bonds will not usually generate the same returns as shares over the long term, but they can help investors stay invested during market downturns.

3. UK Equity or Home Bias Fund.

Some UK investors choose to allocate a portion of their portfolio to domestic companies.

Examples include:

- Vanguard FTSE UK All Share Index

- HSBC FTSE All Share Index Fund

The UK represents roughly 4% of global stock market value, meaning a global tracker already includes UK companies. However, some investors prefer additional exposure to familiar businesses and sterling-denominated assets.

Example Portfolio Allocations.

There is no perfect asset allocation, but the following examples can serve as a useful starting point.

Aggressive Growth Portfolio.

- 90% Global Equities

- 10% Bonds

Suitable for investors with long time horizons and high tolerance for market fluctuations.

Balanced Portfolio.

- 70% Global Equities

- 20% Bonds

- 10% UK Equities

A common choice for investors seeking growth while reducing volatility.

Conservative Portfolio.

- 50% Global Equities

- 40% Bonds

- 10% UK Equities

Often favoured by investors approaching retirement or those uncomfortable with large market swings.

How Much Should You Invest in Bonds?

One of the most debated topics in investing is the appropriate bond allocation.

Historically, a common rule suggested holding a bond percentage equal to your age. However, rising life expectancies and changing market conditions have caused many investors to move away from this approach.

Instead, consider factors such as:

- Time until retirement

- Ability to tolerate losses

- Dependence on portfolio income

- Personal comfort with volatility

If a 30% market decline would cause you to sell investments, a higher bond allocation may be appropriate.

The best portfolio is not necessarily the one with the highest expected return. It is the one you can stick with during difficult periods.

Where Should You Hold Your Portfolio?

UK investors have several tax-efficient account options.

Stocks and Shares ISA.

The ISA remains one of the most attractive investment vehicles available.

Investment growth, dividends and capital gains are sheltered from tax. HMRC statistics show that approximately 15 million adult ISA accounts received subscriptions during the 2023-24 tax year, highlighting the popularity of tax-efficient investing among UK savers.

For long-term investors, a Stocks and Shares ISA is often the first place to build a portfolio.

Self-Invested Personal Pension (SIPP).

A SIPP offers tax relief on contributions and can be particularly attractive for higher-rate taxpayers.

The downside is that funds are generally inaccessible until retirement age, but the tax benefits can be substantial.

Workplace Pension.

For employed individuals, contributing enough to receive the full employer match should usually be a priority.

Employer contributions effectively provide an immediate return on investment that is difficult to replicate elsewhere.

Rebalancing Your Portfolio.

Over time, investment performance will cause allocations to drift.

For example, a portfolio that starts with 80% shares and 20% bonds may become 90% shares and 10% bonds after a strong stock market rally.

Rebalancing restores your desired asset allocation.

Most investors only need to review their portfolio once or twice a year. Frequent adjustments rarely improve results and often lead to unnecessary decision-making.

A simple annual rebalance is usually sufficient.

Common Mistakes to Avoid.

One of the biggest mistakes new investors make is chasing performance.

A fund that performed exceptionally well over the last year may not continue delivering the same results in future.

Another common error is over-diversification. Owning ten different global index funds does not necessarily improve diversification. It often creates unnecessary complexity.

Many investors also underestimate the importance of costs. Even small fee differences can significantly impact returns over several decades. Choosing low-cost index funds can help maximise the portion of returns that remain in your portfolio.

Finally, avoid trying to time the market. Consistently investing through market ups and downs has historically proven more effective than attempting to predict short-term movements.

Simplicity Often Wins.

Building a successful investment portfolio does not require dozens of funds, constant monitoring or expert-level market knowledge. A well-diversified one-fund portfolio or a straightforward three-fund portfolio can provide exposure to thousands of companies worldwide while keeping costs low and management simple.

The most important decision is often getting started. Once your portfolio is established and contributions become automatic, time becomes your greatest ally. Consistent investing, sensible asset allocation and patience have helped generations of investors build long-term wealth, and there is every reason to believe those principles will remain effective for years to come.

Subscribe today and get your free copy of the Investing for Beginners Handbook packed with practical investing tips for UK investors.