Dividend investing has long been one of the most popular ways to build wealth. Whether you own individual shares, investment trusts, exchange traded funds, or income-focused funds, the moment dividends start arriving in your account, a key decision follows. Should you reinvest those dividends to buy more investments, or should you take the cash as income?

There is no single answer that works for everyone. The right choice depends on your age, financial goals, tax position, and whether you are still building wealth or already relying on your portfolio to support your lifestyle.

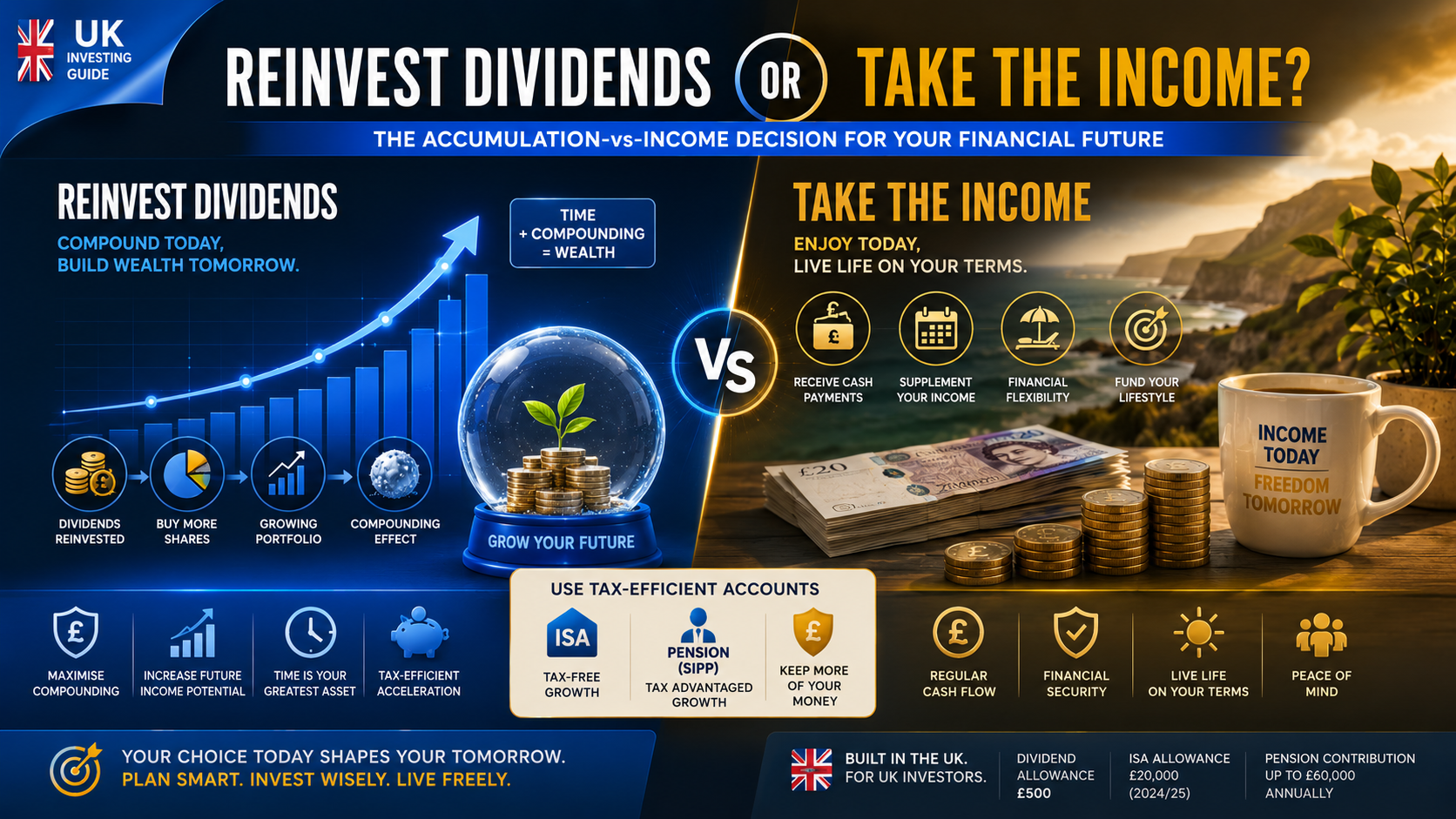

Understanding the accumulation-versus-income decision can have a significant impact on your long-term returns. In many cases, reinvesting dividends can dramatically increase the size of your portfolio over time thanks to the power of compounding.

Why Dividends Matter To Long-Term Investors.

Dividends are payments made by companies to shareholders from their profits. While many investors focus solely on share price growth, dividends have historically accounted for a substantial portion of total investment returns.

A dividend may seem modest at first glance. A portfolio yielding 3% to 5% annually might not appear life-changing in a single year. However, when those payments are consistently reinvested, they begin generating their own returns, creating a compounding effect that can accelerate wealth creation.

This is one reason why many experienced investors view dividends as a powerful contributor to long-term portfolio growth rather than simply a source of spending money.

How Dividend Reinvestment Supercharges Compounding.

Compounding is often described as earning returns on your returns. When dividends are reinvested, they purchase additional shares or fund units. Those additional investments then generate their own dividends, which can be reinvested again.

Over time, this creates a snowball effect.

For example, imagine an investor with £50,000 invested in a portfolio yielding 4% annually. That portfolio would generate approximately £2,000 in dividends during the first year.

If the investor spends the income, the portfolio remains at roughly the same size, assuming no capital growth.

If those dividends are reinvested, however, the investor now owns more shares. The following year's dividend payments are calculated on a larger asset base. Over decades, this seemingly small difference can result in significantly greater wealth.

Investment experts frequently cite dividend reinvestment as one of the key drivers behind long-term stock market returns. Compounding becomes particularly powerful when investors have time on their side.

The Case For Reinvesting Dividends.

For investors still building their portfolios, reinvesting dividends is often the preferred option.

One major benefit is portfolio growth. Rather than relying solely on market appreciation, investors continuously add to their holdings without contributing additional capital from their salary.

Another advantage is discipline. Automatic dividend reinvestment removes emotional decision-making from the investment process. Instead of trying to time markets, investors steadily increase their holdings through good markets and bad.

Reinvestment can also help younger investors maximise the value of tax-efficient accounts such as Stocks and Shares ISAs and SIPPs. Dividends received within these accounts can generally be reinvested without triggering additional UK tax liabilities.

For those pursuing Financial Independence, Retire Early (FIRE), dividend reinvestment is often viewed as a cornerstone strategy because every reinvested pound contributes to a larger future income stream.

When Taking Dividend Income Makes Sense.

While reinvesting is attractive during the accumulation phase, taking dividends as income becomes increasingly relevant later in life.

Many retirees use dividend payments to supplement pensions, State Pension income, or other retirement assets. Receiving regular dividend payments can provide a predictable cash flow without needing to sell investments.

This approach may also appeal to investors seeking greater financial flexibility. Rather than selling assets during market downturns, they can rely on dividend income to help cover living expenses.

Investors approaching retirement often transition gradually from reinvestment to income withdrawals. This creates a bridge between the wealth-building stage and the income-generating stage of their financial journey.

Importantly, there is no rule requiring investors to choose one approach forever. Many switch strategies as their circumstances evolve.

What UK Investors Need To Know About Dividend Tax.

Tax considerations can play an important role when deciding what to do with dividends.

For UK investors holding shares outside tax wrappers, dividend income may be subject to dividend tax once the annual dividend allowance has been exceeded. The dividend allowance currently stands at £500 per year.

However, dividends received within a Stocks and Shares ISA are generally free from UK dividend tax. Likewise, investments held within a pension such as a SIPP can benefit from significant tax advantages.

This makes tax-efficient accounts particularly valuable for investors focused on building long-term dividend wealth.

The annual ISA allowance remains one of the most powerful tools available to UK investors seeking to shelter dividend income and capital growth from taxation.

Dividend Reinvestment And The FIRE Movement.

The FIRE movement has gained popularity across the UK in recent years. The goal is straightforward: save and invest aggressively to achieve financial independence long before traditional retirement age.

Dividend reinvestment often plays a central role in FIRE planning.

During the accumulation phase, investors prioritise growth. Dividends are automatically reinvested, helping portfolios expand faster through compounding.

Once financial independence has been achieved, many investors shift towards generating income from their portfolios. At this stage, dividends may help cover living costs without the need to liquidate investments.

This transition highlights why the reinvest-versus-income decision is not an either-or choice. It is often a strategy that evolves over time.

Accumulation Funds Versus Income Funds.

Investors using funds and ETFs will often encounter two share classes: accumulation and income.

Accumulation funds automatically reinvest dividends back into the fund. Investors benefit from compounding without needing to take any action.

Income funds distribute dividends directly to investors, allowing them to spend the income or manually reinvest it elsewhere.

For investors focused on long-term growth, accumulation funds can offer convenience and simplicity. For retirees seeking regular income, income funds may be the more suitable option.

Choosing between the two often depends on where you are in your investing journey.

Questions To Ask Before Making Your Decision.

Before deciding whether to reinvest dividends or take the income, it is worth considering several important questions.

How many years remain until retirement?

Do you need the income today or can you afford to leave it invested?

Are your investments held within a tax-efficient account such as an ISA or SIPP?

Would reinvesting help you reach your financial goals faster?

Are you building wealth, preserving wealth, or drawing income from wealth?

The answers can provide valuable guidance and help ensure your strategy aligns with your broader financial objectives.

Building A Dividend Strategy For Retirement.

For many investors, dividend reinvestment delivers its greatest benefits during the wealth-building years. By consistently reinvesting income, investors can increase both the size of their portfolio and the future income it can generate.

As retirement approaches, the focus often shifts from growth to sustainability. Dividend payments can become a valuable source of cash flow, helping fund everyday expenses while reducing the need to sell investments.

Rather than viewing reinvestment and income as competing strategies, successful investors often see them as different phases of the same journey. Reinvestment helps build the engine. Income allows you to enjoy the rewards.

The key is understanding where you are today and where you want your investments to take you tomorrow.

Want to learn more about investing? Subscribe today and claim your free copy of the Investing for Beginners Handbook.