Tracker funds have become one of the most popular ways for UK investors to build long-term wealth. With low costs, broad diversification and a straightforward investment approach, they have attracted billions of pounds from investors seeking market returns without the higher fees often associated with active management.

The growth has been remarkable. Tracker funds now account for roughly a quarter of all assets under management in the UK, up significantly from around 18% just five years ago. Passive investing continues to gain market share as investors focus on costs, transparency and long-term performance.

However, not all tracker funds are created equal. Two funds may follow the same index, charge similar fees and appear almost identical on the surface. Yet one may consistently deliver better results than the other. The difference often comes down to a handful of metrics that many investors overlook.

Among the most important are tracking error and fund size. Understanding these factors can help investors identify high-quality tracker funds while avoiding those that may quietly erode returns over time.

Why Tracking Error Matters.

A tracker fund has one primary job. It should follow its benchmark index as closely as possible.

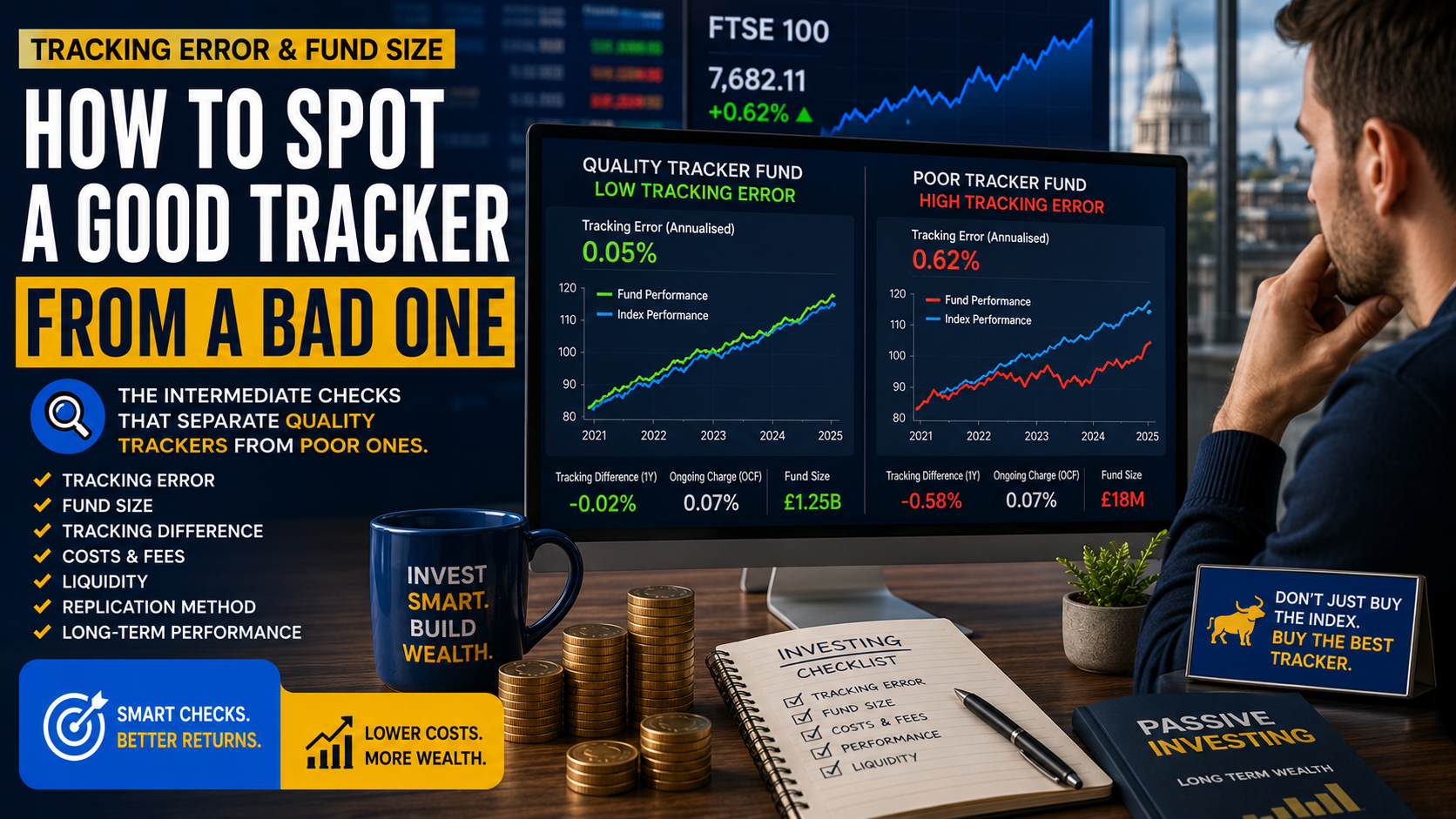

Tracking error measures how consistently a fund follows its index. More specifically, it measures the variability between the fund's returns and the returns of the benchmark over time. A lower tracking error generally indicates that the fund is doing a better job of replicating the index.

For example, imagine a FTSE 100 tracker fund that regularly moves almost exactly in line with the index. Its tracking error would be extremely low. Another tracker may occasionally drift away from the benchmark due to trading inefficiencies, portfolio management issues or cash holdings. That fund would exhibit a higher tracking error.

Many investors focus entirely on annual fees, but tracking error can have a much greater impact on actual returns than a difference of a few basis points in charges.

Tracking Error Versus Tracking Difference.

One of the most common mistakes investors make is confusing tracking error with tracking difference.

Tracking difference measures the actual performance gap between a fund and its benchmark over a specific period. If an index returns 10% and a tracker fund returns 9.7%, the tracking difference is negative 0.3%.

Tracking error, by contrast, measures how consistently that gap changes over time. A fund can have a small tracking difference but still experience a relatively high tracking error if its performance fluctuates unpredictably against the benchmark.

When evaluating tracker funds, investors should examine both figures rather than relying on one metric alone.

What Is Considered a Good Tracking Error?

There is no universal threshold because tracking error varies depending on the asset class and index being followed.

However, for large and liquid equity indices such as the FTSE 100, FTSE All-Share or S&P 500, high-quality tracker funds often maintain tracking errors measured in only a few hundredths of a percent. Some industry research suggests that well-managed large equity ETFs can achieve annualised tracking errors around 0.05% or lower.

Investors should become cautious when tracking error rises significantly above peer group averages without a clear explanation.

A simple rule is to compare multiple funds tracking the same benchmark. The tracker with the lowest and most consistent tracking error often deserves closer attention.

Why Fund Size Can Be a Hidden Advantage.

Fund size is another factor frequently overlooked by retail investors.

At first glance, the size of a fund may seem irrelevant. After all, if two funds track the same index, why should assets under management matter?

In reality, larger funds often benefit from economies of scale that smaller funds struggle to match.

Large tracker funds can spread operating costs across more investors. They generally have better access to liquidity, lower transaction costs and more efficient portfolio management processes. These advantages can contribute to improved tracking performance over time.

The world's largest passive funds demonstrate this trend clearly. Vanguard's S&P 500 ETF recently became the first ETF to exceed $1 trillion in assets, highlighting the growing concentration of assets in highly efficient low-cost trackers.

While investors do not need to choose the biggest fund available, extremely small tracker funds can sometimes present additional risks.

The Risks of Small Tracker Funds.

Smaller funds are not automatically bad investments, but they deserve extra scrutiny.

Funds with limited assets under management may experience wider bid-ask spreads, higher trading costs and lower liquidity. These factors can contribute to larger tracking differences and less efficient index replication.

There is also the possibility of fund closure. ETF providers periodically close products that fail to attract sufficient assets, creating inconvenience for investors who may need to reinvest elsewhere.

As a rough guide, many experienced ETF investors prefer funds with assets above £100 million, although this is not a strict rule and varies by market sector.

The key is understanding whether the fund has achieved enough scale to operate efficiently.

Look Beyond the Ongoing Charge Figure.

Many investors compare tracker funds using only the ongoing charge figure, often known as the OCF.

While costs certainly matter, the cheapest fund is not always the best choice.

Research consistently shows that some funds with slightly higher fees can deliver better tracking results than lower-cost competitors because of superior portfolio management, securities lending programmes or replication techniques.

This means investors should treat fees as just one piece of the puzzle.

A fund charging 0.10% annually but delivering excellent tracking may ultimately provide better value than a competitor charging 0.05% while consistently lagging the index.

Check the Replication Method.

Another useful quality check involves understanding how the fund replicates its index.

Physical replication funds own the underlying securities directly. Full replication funds hold every stock in the index, while sampled funds hold a representative selection.

Synthetic funds use derivatives to replicate performance.

Neither approach is inherently superior, but investors should understand the methodology being used and whether it has historically produced reliable tracking results.

For mainstream UK investors seeking broad market exposure, physically replicated funds are often the simplest and easiest to understand.

Compare Long-Term Tracking Records.

One of the most revealing tests is surprisingly simple.

Look at the fund's performance relative to its benchmark over three, five and even ten years where data is available.

A quality tracker should consistently stay close to its benchmark. Large variations may indicate operational issues, higher hidden costs or inefficient index replication.

Experts increasingly recommend reviewing several years of tracking difference data rather than focusing solely on recent performance. Consistency is often a stronger indicator of quality than a single year's results.

Why UK Investors Are Paying More Attention to Tracker Quality.

The rise of passive investing has transformed the UK investment landscape.

Recent industry figures show tracker funds have grown from around £105 billion a decade ago to approximately £367 billion, representing more than 25% of assets under management.

At the same time, many actively managed funds have struggled to justify their higher fees. Research examining UK-focused pension funds found that roughly nine out of ten underperformed a simple FTSE All-Share tracker over a ten-year period.

As more investors embrace passive investing, selecting the right tracker fund becomes increasingly important. The difference between a well-run tracker and a poorly managed one may appear small in any single year, but over decades those differences can compound into meaningful sums.

The Checklist for Spotting a Quality Tracker Fund.

Before investing in any tracker fund or ETF, consider these intermediate checks:

- Review the fund's tracking error.

- Compare tracking difference over at least three years.

- Assess assets under management.

- Examine the fund's liquidity.

- Compare costs but do not focus solely on fees.

- Understand the replication method.

- Review long-term performance against the benchmark.

- Compare the fund directly with competing trackers following the same index.

These checks take only a few minutes but can help separate genuinely efficient tracker funds from those that merely look attractive on a factsheet.

For investors building long-term portfolios, the goal is not simply finding a tracker fund. It is finding a tracker fund that consistently delivers what it promises: returns that closely match the market with minimal friction, low costs and reliable execution.

Want to build your investing knowledge from the ground up? Subscribe today and claim your free copy of the Investing for Beginners Handbook eBook.