For decades, most retirement planning focused on one simple goal: building the biggest pension pot possible. Yet once retirement arrives, the challenge changes completely. Instead of accumulating wealth, retirees enter what financial planners call the decumulation phase. This is the period when you begin drawing income from your investments and pension savings while trying to ensure the money lasts throughout retirement.

Understanding a safe withdrawal rate can make the difference between enjoying financial freedom and worrying about running out of money later in life. Whether you are approaching retirement, already retired, or pursuing Financial Independence, Retire Early (FIRE), knowing how to generate sustainable income from your portfolio is essential.

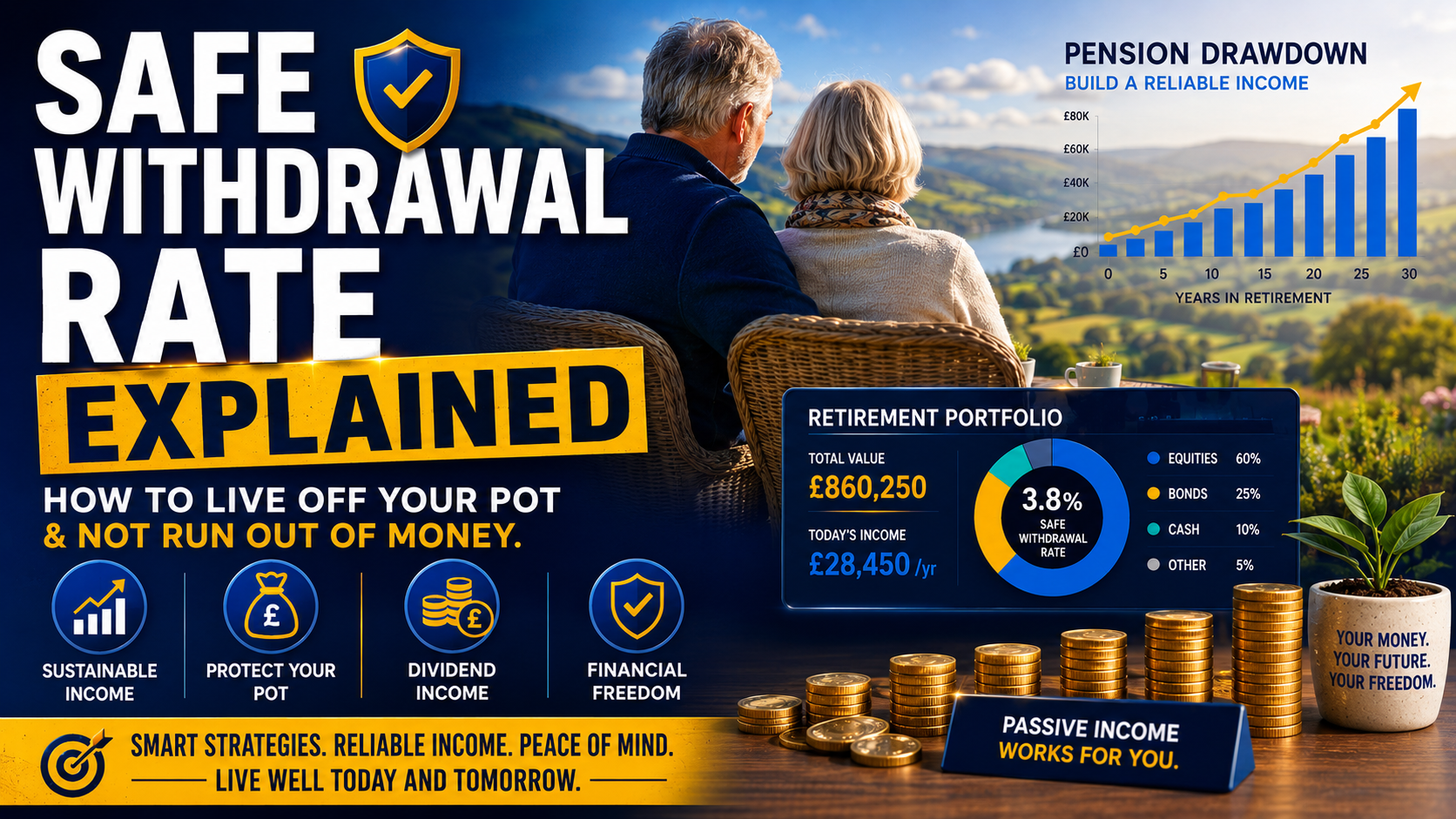

What Is a Safe Withdrawal Rate?

A safe withdrawal rate is the percentage of your investment portfolio that you can withdraw each year while maintaining a high probability that your money will last throughout retirement.

The concept became popular through the famous "4% rule", which suggested retirees could withdraw 4% of their portfolio in the first year of retirement and then increase that amount annually in line with inflation. Historically, this approach was designed to support a retirement lasting around 30 years.

However, retirement planning has evolved significantly. Many experts now believe UK retirees should consider a more cautious approach due to lower expected investment returns, increasing life expectancy and ongoing investment costs. Recent retirement income research suggests a sustainable withdrawal rate for UK investors may be closer to 3.7% to 3.9% rather than the traditional 4% figure.

The exact percentage will depend on factors such as portfolio size, investment mix, spending needs, health and retirement length.

Why Retirement Income Planning Matters More Than Ever.

Retirement is lasting longer than previous generations anticipated. According to recent UK retirement planning data, the average 65-year-old in England and Wales can expect to live to approximately age 85, with many living well beyond that.

That means a retirement lasting 20, 25 or even 30 years is increasingly common.

At the same time, workplace pensions have shifted away from guaranteed defined benefit schemes towards defined contribution pensions, placing more responsibility on individuals to manage their own retirement income.

The Financial Conduct Authority reports that more than 960,000 pension plans were accessed for the first time during 2024/25, highlighting how many people are now making their own retirement income decisions.

The challenge is simple. Withdraw too much and your portfolio may run out. Withdraw too little and you may unnecessarily limit your lifestyle.

Understanding the Decumulation Phase.

The accumulation phase is often straightforward. You save, invest and grow your assets.

The decumulation phase is more complex because several risks emerge simultaneously.

Market volatility can reduce portfolio values. Inflation can erode purchasing power. Unexpected healthcare costs may arise. Longer life expectancy increases the number of years your portfolio needs to support you.

Many retirees also face what experts call "sequence of returns risk". This occurs when poor market performance happens early in retirement. Even if long-term average returns remain strong, large withdrawals during market downturns can permanently damage portfolio sustainability.

This is one reason many retirees adopt flexible withdrawal strategies rather than taking a fixed amount regardless of market conditions.

How Much Income Can Your Pot Generate?

The amount you can safely withdraw depends entirely on the size of your pension and investment portfolio.

Consider these examples using a 4% withdrawal rate:

- £250,000 portfolio = £10,000 annual income

- £500,000 portfolio = £20,000 annual income

- £750,000 portfolio = £30,000 annual income

- £1 million portfolio = £40,000 annual income

Using a more conservative 3.8% withdrawal rate would slightly reduce these figures but may improve long-term sustainability. Recent retirement research suggests a withdrawal rate of approximately 3.8% may be appropriate for larger retirement portfolios.

It is important to remember that these figures usually sit alongside other income sources such as the State Pension, workplace pensions or rental income.

The Role of Dividend Income in Retirement.

Dividend investing remains popular among retirees because it creates a psychological and practical source of income.

When companies distribute profits to shareholders, investors receive dividend payments without necessarily selling their investments. This can help reduce reliance on selling assets during market downturns.

Many dividend-focused investors aim to build portfolios containing established companies with strong histories of paying and increasing dividends over time.

However, relying solely on dividends is not always the optimal strategy.

Dividend payments are never guaranteed. Companies can reduce or suspend dividends during economic downturns. Diversification remains essential.

A balanced retirement portfolio often combines dividend-paying shares, broad index funds, bonds and cash reserves. This approach can provide both income and growth while reducing concentration risk.

For many retirees, dividends form part of the withdrawal strategy rather than the entire strategy.

What Happens If You Withdraw Too Much?

One of the biggest retirement risks is withdrawing income at an unsustainable rate.

Recent reports suggest a growing number of retirees are drawing income at levels significantly above traditional safe withdrawal guidelines. Some retirees are withdrawing more than 8% annually from their pension pots.

While this may be manageable for short periods, consistently withdrawing at high rates increases the likelihood of depleting retirement savings.

For example, a £500,000 portfolio generating average returns of 5% annually may struggle to support withdrawals exceeding 8% for several decades.

Higher withdrawal rates can be particularly dangerous during prolonged market downturns because investors may be forced to sell assets at depressed prices.

Common Retirement Income Strategies.

There is no single approach that works for everyone.

Many retirees use a combination of the following strategies:

Natural Income Strategy.

This approach involves living primarily from dividends, bond interest and other investment income while avoiding selling assets whenever possible.

The advantage is simplicity. The disadvantage is that income levels can fluctuate significantly.

Total Return Strategy.

Investors withdraw a set percentage each year using both investment income and occasional asset sales.

This tends to create more predictable spending patterns and allows for broader diversification.

Bucket Strategy.

Assets are divided into separate "buckets" based on time horizons.

Cash may fund the next two to three years of spending, bonds cover medium-term needs and equities remain invested for long-term growth.

This approach can reduce the emotional impact of market volatility.

Flexible Spending Strategy.

Rather than withdrawing a fixed amount every year, spending adjusts based on portfolio performance.

This can significantly improve the likelihood of maintaining income throughout retirement.

Retirement Lifestyle Expectations in the UK.

One challenge facing many retirees is that pension savings may not stretch as far as expected.

Recent UK pension analysis estimated that an average pension pot of around £152,000 would generate approximately £6,080 annually using a 4% withdrawal rate. Combined with the full State Pension, this would provide around £18,600 per year of retirement income.

While that may support a basic retirement lifestyle, it falls short of the income many people associate with a comfortable retirement.

This highlights the importance of starting early, contributing consistently and maintaining realistic expectations regarding retirement spending.

Is the 4% Rule Still Relevant?

The 4% rule remains one of the most widely recognised retirement planning concepts.

However, it should be viewed as a starting point rather than a guaranteed formula.

Modern retirement planning increasingly focuses on flexibility. Market conditions, inflation, health and personal spending patterns all influence sustainable withdrawal rates.

Some retirees may comfortably withdraw more than 4%, particularly if they have substantial guaranteed income from State Pension or annuities. Others may benefit from a more cautious approach.

The key lesson is that retirement income planning is not a one-time calculation. It requires ongoing monitoring and occasional adjustments.

Building Confidence in Retirement.

Living off your pension pot successfully requires balancing enjoyment today with security tomorrow.

A sustainable withdrawal strategy can help retirees spend confidently without constantly worrying about running out of money. Combining diversified investments, dividend income, sensible withdrawal rates and periodic portfolio reviews can create a retirement income plan capable of supporting decades of financial independence.

Rather than focusing solely on the size of your portfolio, focus on the income it can realistically generate. After all, retirement success is not measured by how much money remains in your account, but by whether it supports the lifestyle you want throughout your later years.

Want to learn more about investing and building long-term wealth? Subscribe today and claim your free eBook, Investing for Beginners Handbook.