Cryptocurrency and index funds are often presented as competing investment choices. One promises potentially life-changing gains through emerging technology, while the other offers steady wealth building through broad market exposure. For many investors, especially those just starting out, the question is simple: where should long-term money actually go?

The answer is not as straightforward as crypto supporters or passive investing advocates might suggest. Both asset classes can play a role in a portfolio, but they serve very different purposes. Understanding their track records, volatility, risk profiles and long-term potential is essential before deciding where your money belongs.

Why This Debate Matters More Than Ever.

The popularity of cryptocurrency remains significant in the UK. According to research from the Financial Conduct Authority (FCA), around 12% of UK adults owned crypto assets in 2024, equivalent to roughly seven million people. Average holdings also increased, showing that investors continue allocating meaningful amounts of capital to the sector.

At the same time, index funds remain one of the most widely recommended investment vehicles for building long-term wealth. Funds tracking broad markets such as the FTSE All-Share, S&P 500 or global stock indices provide investors with exposure to hundreds or thousands of companies through a single investment. The FTSE All-Share alone captures approximately 98% of the UK's market capitalisation.

As more investors seek financial independence, passive income and retirement security, comparing crypto and index funds has become increasingly relevant.

Understanding What You Are Actually Buying.

One of the biggest differences between crypto and index funds is what investors actually own.

When investing in an index fund, you are purchasing a share of real businesses. Whether it is Apple, Microsoft, Unilever, AstraZeneca or thousands of other companies, your investment represents ownership in organisations that generate revenue, employ people and produce profits.

Cryptocurrency is fundamentally different. Most cryptocurrencies do not produce earnings, pay dividends or generate cash flow. Their value is largely determined by market demand, adoption and investor sentiment.

Bitcoin, for example, is often described as digital gold because of its limited supply. While many investors believe it can act as a store of value, it does not produce income in the same way that businesses can.

This distinction is important because long-term investment returns often depend on underlying economic productivity. Companies can grow profits over time. Cryptocurrencies depend primarily on future demand exceeding current demand.

The Track Record Comparison.

When assessing long-term investments, historical performance matters.

Global stock markets have delivered positive long-term returns for more than a century. While annual results vary, diversified equity portfolios have historically generated average returns of approximately 7% to 10% per year over long periods after inflation, depending on the market and timeframe.

The FTSE All-Share remains one of the most commonly used benchmarks for UK investors and serves as the foundation for many passive investment strategies.

Cryptocurrency has produced some extraordinary gains during its relatively short history. Bitcoin has risen from fractions of a penny to becoming one of the world's largest financial assets. Early investors achieved returns that traditional markets could never realistically match.

However, crypto's track record is much shorter. Bitcoin has existed since 2009, while stock market data spans generations. Investors considering long-term wealth building should recognise that a decade of performance is very different from a century of evidence.

Volatility Is Where The Biggest Difference Appears.

Perhaps the most important distinction between crypto and index funds is volatility.

Stock markets can experience significant declines. The 2008 financial crisis, the Covid-19 market crash and various economic downturns all created periods of substantial losses. However, diversified stock markets have historically recovered and gone on to reach new highs.

Cryptocurrencies frequently experience much larger swings.

Bitcoin has repeatedly fallen by more than 50% during market downturns. Other cryptocurrencies have suffered declines of 80% to 90% or more. For investors who struggle emotionally with volatility, these moves can lead to panic selling and poor decision-making.

The practical consequence is that many investors underestimate how difficult it is to hold crypto during major market crashes. A portfolio that loses 70% of its value requires gains of more than 230% simply to break even.

For most people saving for retirement, a house deposit or long-term financial goals, such extreme volatility introduces additional risk.

The Case For Index Funds.

Index funds have become the cornerstone of modern passive investing for several reasons.

First, they provide instant diversification. Instead of relying on the success of one company or sector, investors spread risk across hundreds or thousands of businesses.

Second, costs are typically very low. Many index funds charge annual fees well below 0.25%, allowing investors to keep more of their returns.

Third, index funds require very little maintenance. Investors can contribute regularly, reinvest dividends and allow compound growth to work over decades.

Research consistently shows that many actively managed funds fail to outperform broad market indices over long periods after fees are considered. This has strengthened the case for passive investing among both professional advisers and retail investors.

If you want a deeper understanding of why millions of investors favour this approach, see our guide to Index Funds & Passive Investing, where we explain how low-cost investing can help build wealth over time.

The Case For Cryptocurrency.

Despite the risks, crypto continues attracting investors for several legitimate reasons.

Supporters argue that blockchain technology could reshape financial services, payments and digital ownership. Bitcoin enthusiasts view the asset as a hedge against currency debasement and government monetary policies.

Crypto also offers potential growth that mature stock markets may struggle to match. While a diversified stock market portfolio might generate single-digit annual returns over the long term, successful crypto investments can occasionally produce dramatically larger gains.

The challenge is identifying which cryptocurrencies will survive and thrive over the coming decades. Thousands of digital assets have already disappeared, while only a handful have achieved widespread adoption.

Investors should recognise that crypto often behaves more like a speculative asset than a traditional investment.

What UK Investors Should Know About Tax.

For UK investors, tax considerations can influence investment decisions.

Index funds held within Stocks and Shares ISAs allow investments to grow free from capital gains tax and dividend tax. Pension accounts such as SIPPs offer additional tax advantages for retirement savings.

Cryptocurrency investments generally do not enjoy the same protections when held directly. Capital gains tax may apply when disposing of crypto assets, depending on individual circumstances and allowances.

As UK regulation evolves, investors should remain aware of changing rules and reporting requirements. Seeking professional advice may be worthwhile for larger portfolios.

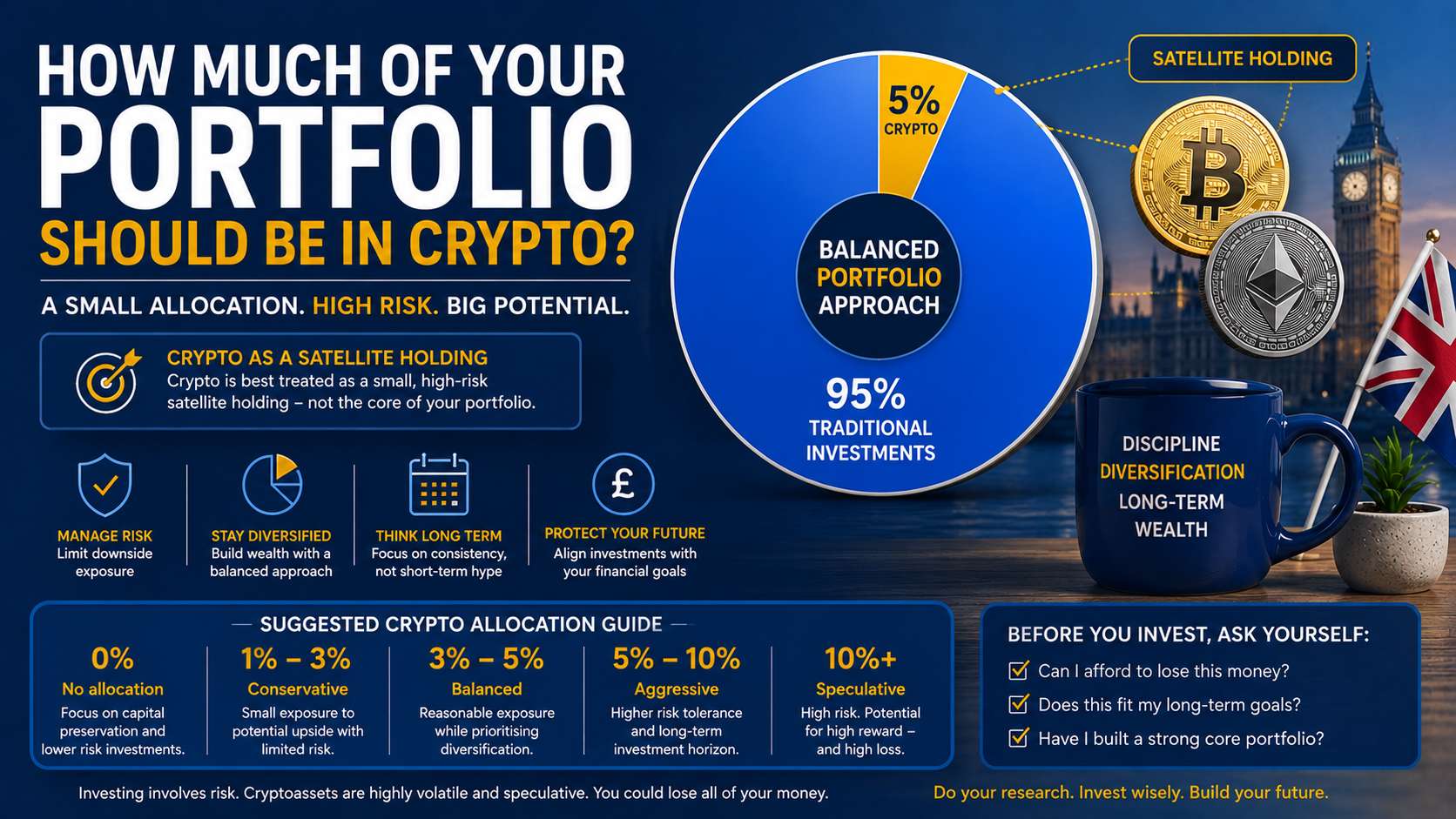

Can Crypto And Index Funds Work Together.

Many investors frame the discussion as an either-or decision when it does not necessarily need to be.

A growing number of long-term investors use a core-and-satellite approach. The majority of their portfolio sits in diversified index funds, while a smaller percentage is allocated to higher-risk opportunities such as cryptocurrency.

For example, an investor might place 90% of their capital into global index funds and 10% into crypto. This allows participation in potential upside while limiting the impact of severe losses.

The appropriate allocation depends on individual risk tolerance, investment horizon and financial objectives.

Which Option Is Better For Long-Term Wealth Building.

For most investors focused on retirement, financial independence and long-term wealth accumulation, index funds remain the more reliable foundation.

They offer diversification, lower volatility, proven historical performance and strong tax-efficient investing opportunities within UK accounts such as ISAs and pensions.

Cryptocurrency may still have a place for investors who understand the risks and are comfortable with substantial price fluctuations. However, it should generally be viewed as a speculative component rather than the foundation of a long-term financial plan.

The most successful investors often prioritise consistency over excitement. Building wealth slowly through regular contributions to diversified investments may not generate headlines, but history suggests it remains one of the most effective strategies available.

Want to build a solid investing foundation? Subscribe today and get your free copy of the Investing for Beginners Handbook eBook delivered straight to your inbox.